The Puerto Rico Electric Power Authority (PREPA) filed for debt restructuring on July 2, 2017, under Title III of the Puerto Rico Oversight, Management, and Economic Stability Act (PROMESA). The case is administered by the U.S. District Court for the District of Puerto Rico, with Judge Laura Taylor Swain presiding. Title III proceedings are bankruptcy-adjacent but are not governed directly by the U.S. Bankruptcy Code; the judge applies select provisions of federal bankruptcy law, incorporated by reference into PROMESA, to the U.S. territory’s public debtors. Under this structure, Puerto Rico has found that declaring bankruptcy is expensive. Total advisory and professional fees paid to attorneys, financial advisors, and consultants across all parties in all Title III proceedings under PROMESA have now surpassed $1.5 billion, a figure that sets a record for a municipal restructuring of this type.

PREPA’s case is the last major outstanding Title III restructuring. As we enter the ninth year of the never-ending saga known as the PREPA Title III case or bankruptcy process, and sure as winter turns to spring, there is no agreement yet between the Fiscal Oversight and Management Board (FOMB) and PREPA’s major creditor groups, including its bondholders.

Why a Reasonable Settlement is Important

Rebuilding and modernizing Puerto Rico’s electric power system represents one of the most complex institutional, financial, and technical challenges currently facing any U.S. jurisdiction. Nearly a decade after Hurricane Maria devastated the island’s grid in September 2017, and almost nine years into PREPA’s Title III bankruptcy proceeding, the system remains trapped in a web of mutually reinforcing structural contradictions that no single reform has successfully addressed.

The Puerto Rico electric power system consists of six critical subsystems: (1) the restructuring of PREPA’s financial obligations; (2) the reconstruction of the damage caused to the grid by Hurricane Maria; (3) the transition to 100% renewable generation by 2050, as mandated by Puerto Rico law; (4) the operation of the transmission and distribution (T&D) grid pursuant to the terms and conditions of the LUMA T&D operation and management agreement; (5) the operation of the PREPA legacy generation fleet pursuant to the terms and conditions of the Genera PR operation and management agreement; and (6) the drafting and implementation of the Integrated Resource Plan (IRP) for the entire electric system.

These six subsystems are not independent policy challenges or technical tasks that can each be solved in isolation from the others. Collectively, they form a tightly connected system with reinforcing feedback loops and critical balancing mechanisms, which oftentimes interact in a nonlinear, dynamic way that inevitably produces outcomes at variance with stated policy objectives. In the context of Puerto Rico’s electricity sector policy, these concepts explain why standard policy tools —rate design, capacity expansion, regulatory standards— often fail to produce the intended effects. The Title III case impacts them all.

When analyzing potential settlement deals with bondholders, it is necessary to keep in mind the following:

- The Puerto Rican economy and the Puerto Rico electric system interact with each other. Affordable, reliable electric power is necessary, but not sufficient, to generate sustainable economic growth. Higher economic growth, in turn, increases employment and demand for electricity, which requires new investment to meet the additional demand, which eventually supports additional economic activity, which further increases employment and economic growth, and so on. This cycle also works in reverse: when power costs are high or electric service is unreliable, economic activity contracts, employment decreases, and demand for electricity declines. A downturn in demand for electricity, if permanent, creates a difficult situation as the operator still has to generate sufficient revenues to operate the system, leading to increases in rates, which in turn put downward pressure on employment and economic activity, further decreasing demand for electricity. Any proposed settlement with PREPA’s bondholders has to take into account this interactive relationship between the island’s economy and the cost of electricity.

- In addition, Puerto Rico has approximately $13.5 billion available in FEMA Public Assistance obligations for grid reconstruction, with total federal allocations exceeding $16 billion across all programs, most of which remains unspent. A swift and reasonable settlement of PREPA’s bankruptcy would theoretically restore market confidence and allow PREPA to leverage federal funds with private co-investment. A prolonged dispute or full repayment would destroy this leverage.

- The prolonged bankruptcy has also been a headwind on new investment in renewable energy generation at the utility scale-level. Most private investors seeking to finance a new solar farm with a power purchase and operating agreement (PPOA) with PREPA would be quite reluctant, and reasonably so in our opinion, to execute a long-term agreement with a bankrupt entity. The Title III case, therefore, is effectively a bottleneck slowing down new private sector investment in renewable generation at scale. This is important because if Puerto Rico currently generated, say, 40% of all its electricity using utility-scale solar generation, it would produce materially significant net savings on fuel expenditures that could then be passed on to ratepayers. Replacing current fossil fuel generation, which has a highly variable cost dependent on events affecting the global fuel markets, with lower, fixed cost utility-scale renewable generation would (1) permanently decrease PREPA’s fuel expense and, everything else being equal, (2) significantly improve PREPA’s operating margin, which would provide headroom for significantly lowering customer rates.

- The long-term planning for the system has also been affected by the long-running bankruptcy procedures. It is difficult to plan large expenditures for fixed investments with a long useful life if the planners do not know how much of PREPA’s outstanding legacy debt would have to be paid and on what terms, and if future access to the capital markets remains uncertain. The IRP is the master planning document for the electric power system, covering a 20-year planning horizon. The 2019 IRP, prepared by Siemens, recommended aggressive renewable deployment, grid decentralization through mini-grids, and phased retirement of fossil fuel assets. The 2025 IRP, currently in development by LUMA with interim filings in November 2024 and February 2025, represents the first comprehensive update since LUMA assumed T&D operations. The IRP’s recommendations regarding capital investment, decommissioning timelines, adoption of new generation technologies, and rate trajectories will all be significantly influenced by the PREPA bankruptcy settlement.

- Finally, an unreasonable bankruptcy settlement could spark a Rate-Revenue Death Spiral. Elevated electricity rates (driven by high fossil fuel costs and debt service requirements) increase the economic incentive for customers to reduce their consumption through energy efficiency or to exit the grid entirely through distributed renewable generation, particularly rooftop solar. This grid avoidance reduces the load volume that PREPA must serve, eroding its total revenue. To maintain sufficient revenue for debt service and operations, PREPA must increase rates further, which accelerates grid avoidance. The cycle reinforces itself, with rates rising faster than demand falls, eventually reaching a point where the most efficient investment for a customer is to exit the grid entirely.

- The Rate-Revenue Death Spiral has policy implications that extend beyond financial sustainability. As rates increase, residential customers with capital (typically higher-income households) invest in distributed solar and battery storage, while renters and lower-income homeowners who cannot make the upfront investment bear the burden of rate increases. This creates a regressive distributional outcome: lower-income customers subsidize the energy independence of higher-income customers. Moreover, customers who exit the grid through distributed generation retain backup service from the utility, effectively requiring the remaining customers to finance infrastructure that serves the departed customer’s occasional needs.

State of Play

Last time we checked with our protagonists, the bondholder groups were celebrating a November 2024 ruling from the First Circuit Court of Appeals in Boston which held, among other things, that bondholders held an $8.5 billion claim (plus accrued interest and fees) secured by a properly perfected lien on PREPA’s past, present, and future net revenues, as opposed to being secured only by funds deposited in certain PREPA accounts. According to some analysts, this ruling has fundamentally altered the negotiating dynamic. Yet, as of this writing and to the best of our knowledge, it has not been fully incorporated into a revised Plan of Adjustment.

We note, however, that the phrase “among other things” is carrying a lot of weight in that sentence, because the First Circuit also held that (1) even though bondholders could make a claim in the amount of $8.5 billion, that does not mean they would actually recover that amount in full; their recovery is, instead, contingent on PREPA’s future net revenues, if any; and (2) bondholders had no recourse, other than PREPA’s net revenues, as their source of repayment. This latter holding is extremely important because it means bondholders cannot seek recovery from any other PREPA assets or from any other Puerto Rico government sources, such as the general fund. The FOMB, thus, also had reason to celebrate the ruling.

In early August, President Trump removed six of seven sitting Oversight Board members. Judge Swain then suspended all case deadlines on August 8, 2025, and ordered the Board to report on its operational status. The suspension effectively froze proceedings for several months. Eventually, three of the removed board members were reinstated by a federal court. The Trump administration has announced its intention to appeal this decision, but is waiting for the court system to rule on a similar dispute before taking further action regarding the FOMB (at least for now).

Boundaries of a Potential Settlement with Bondholders

So, given this state of play, what are the boundaries of a potential settlement with bondholders?

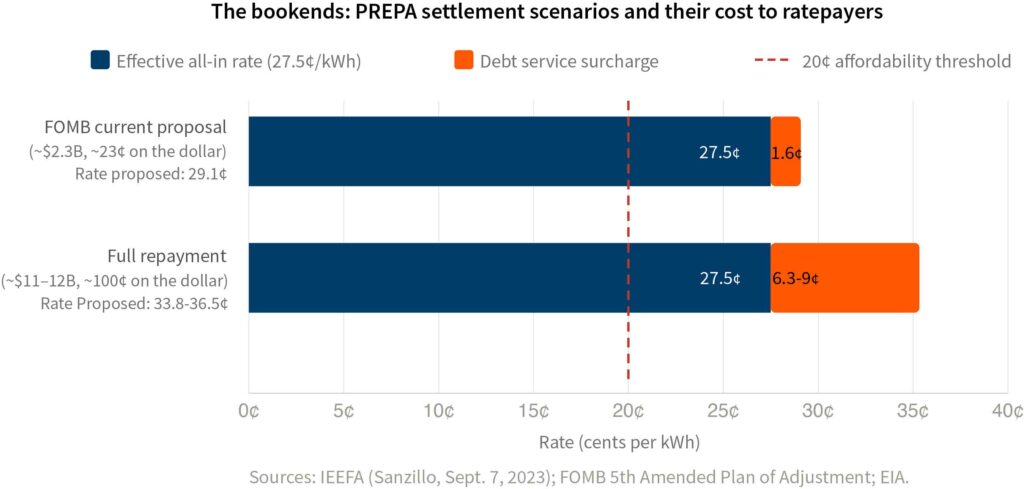

PREPA currently charges approximately 27.5 cents per kWh (including active Puerto Rico Energy Bureau -approved temporary surcharges as of late 2025 of 1.92 cents for pension payments and 1.49 cents for operating expenditures), already among the highest utility rates in the United States and significantly above the 20 cents per kWh affordability threshold recognized by both the Puerto Rico Legislature and the FOMB. Puerto Rico’s median household income is approximately $25,000 (2023 ACS) — roughly one-third the U.S. mainland median — and approximately 40% of residents live below the federal poverty line. The island’s economic activity index has contracted or stagnated since 2024, reflecting a difficult environment that severely limits the economy’s capacity to absorb rate increases.

PREPA generates approximately 19–20 billion kWh of electricity annually (EIA/CRS 2023). Given declining population and ongoing customer defection to rooftop solar, this volume is expected to decrease over a 35-year bond amortization period. A $1 billion debt obligation, financed over 35 years at 4.5–5%, generates annual debt service requirements of approximately $57–61 million, which translates to a rate surcharge of roughly 0.29–0.32 cents per kWh based on current consumption levels. This surcharge does not include any other charges that would be necessary to finance an estimated $6 billion in additional capital spending required to modernize the grid and which is not covered by currently available federal funding.

Based on those assumptions, we believe there are two “bookend” scenarios that determine the universe of potential settlement agreements with bondholders.

The low-end scenario is bounded by the Oversight Board’s current proposed range (23 cents recovery under the 5th Amended Plan). The FOMB’s revised plan, which proposed $2.3 billion in new bonds (representing roughly a 23% recovery), was projected by the Institute for Energy Economics and Financial Analysis (IEEFA) to add approximately 1.6 cents per kWh to customer bills over 35 years, costing ratepayers a total of roughly $5.1 billion (Sanzillo, IEEFA, Sept. 7, 2023). Under this scenario, PREPA would still be required to raise additional capital for grid investment, likely from a market that views any new indebtedness as deeply subordinated to the bonds issued to exit the Title III proceeding because bankruptcy exit bonds would presumably be secured with a first lien on PREPA’s net revenues.

This scenario is perhaps the most realistic and favorable for Puerto Rico ratepayers and the grid investment program, but creditors relying on the First Circuit lien ruling are unlikely to accept it absent further litigation losses.

At the other end of the spectrum, full repayment of the face value of PREPA’s bonded debt — plus post-petition interest, administrative claims, and fees, as the holdout coalition contends — would produce a total obligation of approximately $11–12 billion. This scenario is not considered economically feasible by most parties to the proceeding, including Judge Swain, who has publicly characterized some of the bondholders’ arguments as “likely delusional” (Slavin, Judge pushes PREPA, creditors to negotiate deal in 60 days. Bond Buyer. July 11, 2024).

A recovery in the order of $9–12 billion would require rate surcharges probably in the range from 6.3 to more than 9 cents per kWh, producing a new blended rate of 34–37+ cents per kWh. This plan would almost certainly be non-confirmable under PROMESA’s feasibility standard: at rates this high, customer defection to rooftop solar accelerates, the revenue base erodes faster than debt is serviced, and PREPA’s balance sheet becomes permanently insolvent, making it impossible for PREPA to perform under the plan without re-defaulting. Population flight and eventual system collapse would further hollow out the very revenue base on which any settlement’s long-term sustainability depends.

Conclusion

The PREPA Title III case is approaching a critical decision point. The November 2024 First Circuit ruling has given a second wind to bondholders, and the Oversight Board faces the challenge of crafting a confirmable plan that respects creditor rights while preserving Puerto Rico’s economic viability.

This is admittedly a difficult needle to thread. Pay too little and the economic impact is manageable, but the settlement is likely to be contested for years, and the capacity to issue new debt to fund grid capital investments in the future is, in the best case, constrained. Offer too much and the legal viability of the plan is compromised — and in the unlikely event such a plan is confirmed, its impact on the economy of Puerto Rico could be devastating while eliminating any possibility of future grid investment capacity.

In the end, the single most consequential variable is time. Every year that PREPA remains in bankruptcy is a year in which grid investment is deferred, federal incentives go unused, costly litigation drags on, the transition to renewables is delayed, work on the master IRP stalls, and the island’s population and economic base continue to erode — reducing the very revenue base that is expected to service PREPA’s restructured debt. A swift, pragmatic settlement may ultimately be less costly to Puerto Rico’s economy than the continued damage of delay.